December 26, 2025 · 8 mins read

Santosh Kumar

A ₹2,000 FD-based credit card is the easiest and most secure way to kickstart your credit journey in India. It’s available, low risk and targeted at individuals who might not be eligible for a traditional credit card because they can’t provide proof of income or a credit history. Although these cards are typically less expensive than unsecured credit cards, they aren’t cost-free.

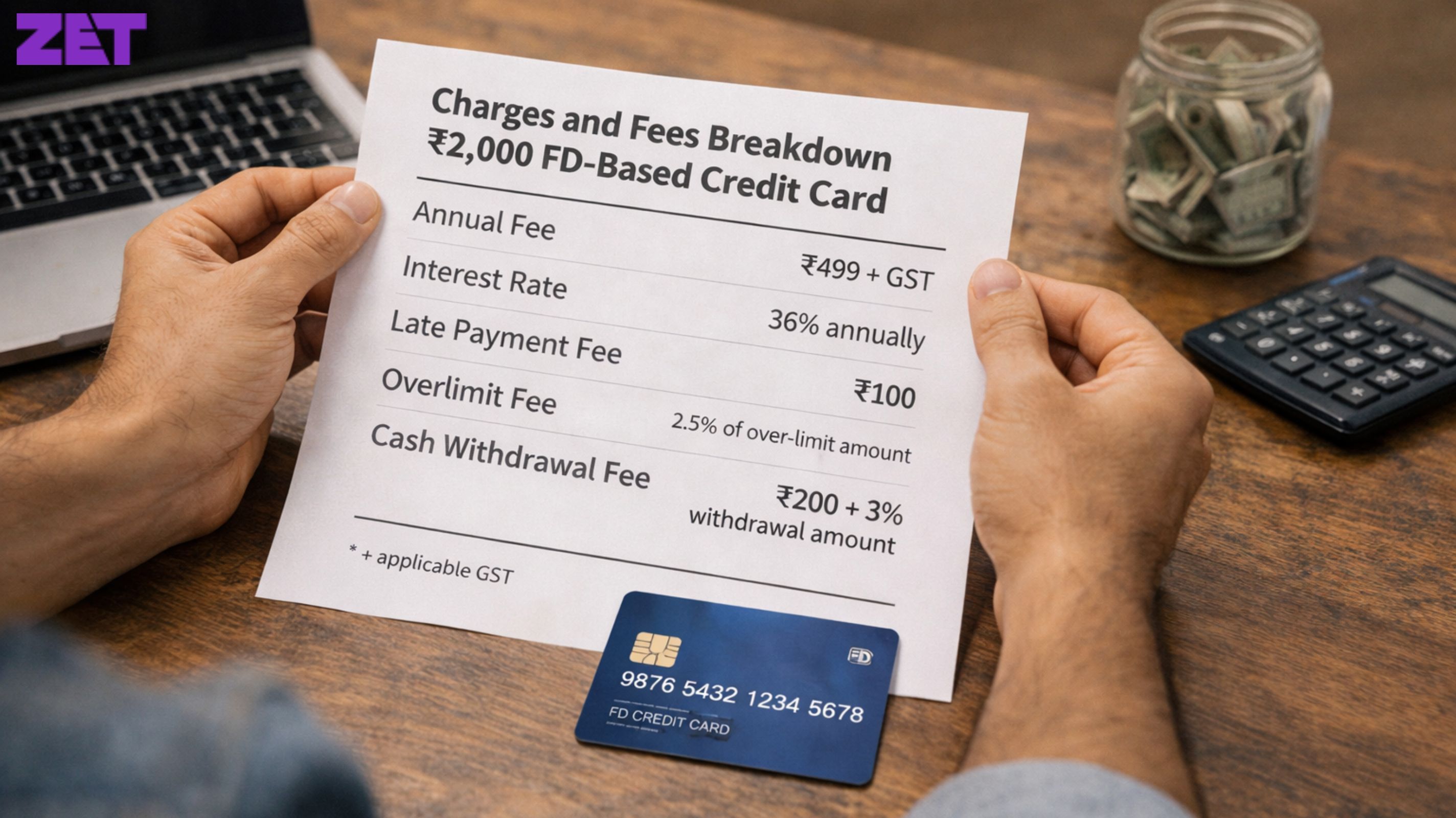

Understanding the 2000 FD credit card charges in advance helps you avoid surprises and make smarter decisions. Too many users pay attention exclusively to eligibility and approval, the real value of a credit card, however, is in how well you understand and how carefully you manage its fees.

And since the credit limit is tiny, even small fees can sting. A late payment or interest charge can quickly consume your available limit, leaving the card useless. That is why understanding secured credit card fees in India is especially important for beginners.

FD-based cards are beginner-friendly, but they still play by credit card rules. Fees are in effect when you fail to satisfy certain conditions, and being aware of these conditions ahead of time keeps you in the driver's seat.

Also Read: How to Apply for a ₹2,000 FD Credit Card on ZET App: A Step-by-Step Guide?

The first thing is to understand that the FD is not a fee. The ₹2,000 you put in is still your money. But of course, there’s an opportunity cost.

Your cash remains tied up in the FD for the entire duration that the credit card is valid. Although you do accrue interest on the deposit, it tends to be modest. Relative to the freedom of cash in hand, this can seem like a hidden tax.

Yet for most newbies, this compromise is worth it for the opportunity to establish credit.

Also Read: Can Students Get a ₹2,000 FD Credit Card? A Complete Guide

Most ₹2,000 FD credit cards have zero joining and annual fees as well. That’s one of their great benefits. Banks realise these cards go after rookies, so they tend to waive these fees entirely.

But not all cards are structured the same way. Others will charge a nominal yearly fee, particularly if the card has special benefits or incentives. n) Always verify if the card is lifetime free or free for a year only.

A small annual fee seems huge when your credit limit is just $2,000, so this is definitely something to verify prior to applying.

Also Read: How a ₹2,000 FD Credit Card Helps Build Your CIBIL Score Fast

And interest charges if you don’t pay your full bill by the due date. This is also where a lot of users inadvertently lose money.

FD-based credit cards have interest rates akin to regular credit cards. They can be as high as thirty to forty per cent a year. On a minor cap, this can still accumulate rapidly if balances carry over. The surest path to steering clear of interest altogether is to pay off your full balance every month. FD-based cards are better treated as a charge than as borrowing tools.

Late payment fees hit if you miss or pay under the minimum. These fees differ from bank to bank, but generally start from a few hundred rupees onwards.

On a ₹2,000 limit card, even a small late fee feels heavy. Even worse, late payments ding your credit score, which undermines the primary motivation for the card. Reminders or auto-debit can prevent this charge altogether.

Also Read: ₹2,000 FD Credit Card Limit: How Much Limit Can You Get?

While most FD-based credit cards permit cash withdrawals, avoid them like the plague unless inevitable.

Cash advance fees are typically a fraction of the amount, plus instant interest from the day of withdrawal. It does not offer an interest-free period on cash advances.

This is one of the most common low FD credit card hidden charges that users overlook. It defeats the purpose of your card to take it for cash, and it costs a whole lot more.

Also Read: Best Credit Cards In India You Can Get On A ₹2,000 FD (2026 List)

If your card has international capabilities, overseas currency fees are possible. These usually fall between 2-3% of the value being transacted.

For the ₹2,000 FD cardholders, international spending is uncommon; however, online subscriptions or minor digital purchases occasionally activate these fees.

Making sure international use is on and knowing the fee structure can save you some surprise deductions.

Also Read: How to Get a Credit Card with Just a ₹2,000 FD in India

FD-based cards generally can’t spend more than the authorised limit. Instead of over-limit fees, transactions can just be declined.

Though this bypasses additional fees, multiple declines are bothersome. Monitoring your available limit and pending transactions keeps this from happening.

A few banks impose a nominal fee for card replacement if it is lost or damaged. Fees could also be incurred for paper statements, reprinted bills or select service inquiries.

These fees are generally small but nonetheless should be taken into account, particularly for budget users.

Also Read: How to Create a UPI QR Code for Your Shop or Business?

The ZET Credit Card platform focuses on clarity and transparency, especially for users new to credit. Although the card itself is issued by partner banks, ZET makes sure users know where charges apply before and after onboarding.

For FD-based cards, ZET focuses on responsible usage over aggressive spending. The platform aids users in tracking dues, billing cycles and avoiding fees. It also allows newbie cardholders to grow credit without fee traps.

Also Read: How to solve ‘UPI ID Not Found’ error?

The easiest way to bring down the cost is to approach the card as a lesson, not a loan. Use sparingly, shave in full and skip cash advances.

Checking your statement regularly makes sure you catch any surprises early. A lot of users are caught unaware by fees because they didn’t check their statement for the month. It’s discipline, not features, that makes these cards valuable.

Also Read: UPI vs Wallet Payments: Which One Should You Use?

In many ways, yes. FD-based cards typically offer lower or no annual fees and more accessible approval. But interest rates & penalties are just like unsecured cards.

Where you really save is in users spending less because of the low limit. To which, of course, inherently minimises the risk of falling into debt.

If an FD-based card has expensive annual fees or convoluted service charges, it might not be worth opting for. With so many newbie-friendly picks, why settle for a card with confounding costs?

Don’t just compare eligibility – always compare fees.

Also Read: What Is UPI 123Pay and How to Use It Without Internet?

If fees are considered in long-term value. Even if you pay a few dollars in fees along the way, but establish a great credit score that makes it easier to access superior financial products down the road, it’s well worth it.

The trick is to make certain that charges are occasional and controllable as opposed to frequent and preventable.

There are no sneaky fees. Read the fine print, but interest,late fees and cash withdrawal fees can feel sneaky if you are unprepared.

Most are free forever, but a few can charge a small yearly fee depending on the bank and card features.

Yes, interest is applicable if you fail to settle the complete amount due by the deadline.

Very occasionally, in cases where non-payment is sustained for a period of time, banks may recover dues from the FD, but again, this is typically only after repeated default.

It potentially can be cheaper for beginners because of the lower fees and spending controls; however, abuse can still run up high costs.

ZET itself is free from hidden fees and transparent about its pricing, though bank-level charges still apply.

Pay your bill in full each month, skip cash advances and monitor your due dates.

Contact

care@zetapp.in

Social

Build and Maintain a 750+ Credit Score