March 11, 2026 · 5 mins read

Santosh Kumar

Loan closure and loan settlement are two different ways of closing a loan account in a credit report. Loan closure means the borrower has repaid the entire outstanding amount according to the agreement. Loan settlement means the borrower paid only part of the outstanding amount after negotiating with the lender, which may negatively affect the CIBIL score.

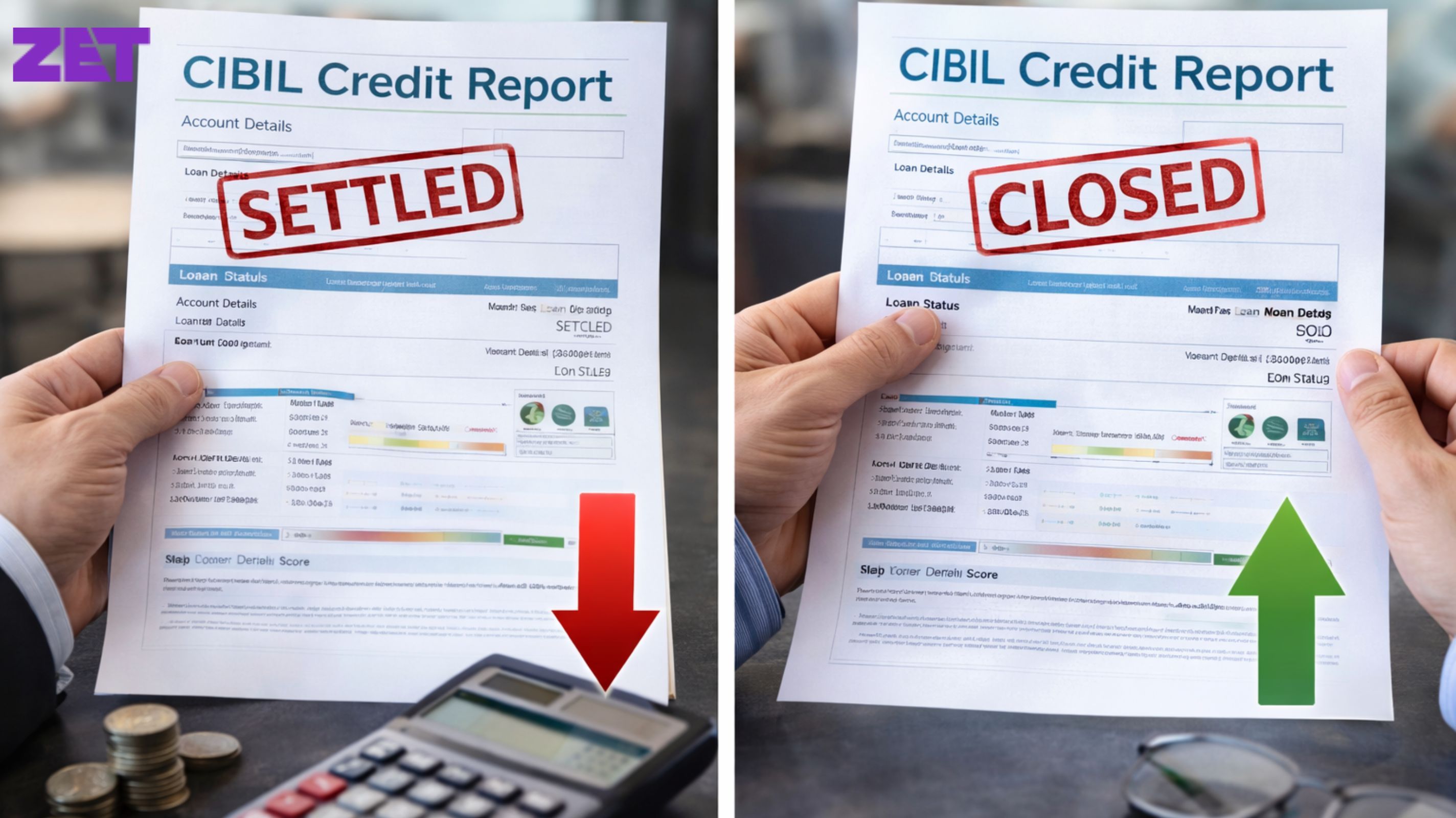

Loan closure refers to the circumstance wherein a borrower repays the entire loan amount, interest and charges as per the repayment schedule. Once the final instalment is paid, the lender marks the account as “Closed” in the credit report maintained by TransUnion CIBIL.

A closed loan signifies good credit habits. It means the borrower repaid his debts and respected the loan contract. This also looks good to banks and lenders for future loans.

Say, for instance, a borrower has a three-year personal loan and pays every due instalment on time up until the last payment, then the loan is reported as closed. That kind of history keeps a credit record in good standing, and can even raise a credit score.

Loan settlement typically occurs when a borrower is in financial distress and cannot repay the full loan. In which case the borrower can often work out a deal with the lender to pay a smaller amount to close the account.

When the lender accepts this reduced payment, the account is marked as “Settled” in the credit report instead of closed. Although the debt is technically satisfied, the history illustrates that the borrower did not repay the entire initial sum.

From a lender’s point of view, that translates to increased credit risk. Therefore, loan settlement can reduce the borrower’s CIBIL score and make it more difficult to get new loans or credit cards in the future.

Factor: Meaning

Loan Closure: Full repayment of loan as per agreement

Loan Settlement: Partial repayment after negotiation

Factor: Credit Report Status

Loan Closure: Marked as “Closed”

Loan Settlement: Marked as “Settled”

Factor: Impact on CIBIL Score

Loan Closure: Positive or neutral

Loan Settlement: Negative impact

Factor: Future Loan Approval

Loan Closure: Easier to obtain credit

Loan Settlement: Lenders may hesitate

Factor: Borrower’s Financial Image

Loan Closure: Shows financial discipline

Loan Settlement: Indicates repayment difficulty

Loan closure typically benefits a robust credit profile due to the display of steady repayment habits. Regular payments benefit the borrowers reputation and credit history.

Loan settlement, on the other hand, indicates that the borrower couldn’t afford to stick with the original terms. As a consequence, the borrower’s score might drop, and lenders might approach future loan applications with caution. The settlement note can linger on the credit report for a number of years, though it’s impact diminishes over time with good credit habits.

In certain instances, borrowers attempt to change a settled account to a closed account. This, at least occasionally, can be accomplished by settling the outstanding balance to the lender.

Once the amount is paid off, the borrower can ask the lender to report it as settled with TransUnion CIBIL. If the lender agrees, the account can be reported as closed rather than settled, which can bolster the borrower’s credit profile.

But this alternative is contingent on the lender’s internal policies, and may not be widely available.

Also Read: Annual Fee vs Lifetime Free Cards

Make all credit and loan instalments on time. Payment history is a huge way to increase credit scores.

Don’t go overboard on taking loans or apply for several loans at a time. Responsible credit usage shows discipline.

If you use credit cards, aim to maintain utilization under 30 percent of the available limit. Lower utilization bolsters the credit profile.

Also Read: What is UPI 2.0?

With monitoring from TransUnion CIBIL, you can track your progress and that everything is accurate.

However, with responsible lending practices, borrowers can recover their creditworthiness over time post-settlement.

Loan closure and loan settlement both close out a loan account, but they have very different impacts on a borrower’s credit history. Loan closure accounts for responsible repayment and contributes to a robust credit history.

A settlement may not permanently damage your credit score, but it will appear on the credit report for several years. Over time, if you demonstrate responsible credit behaviour to other lenders, this will improve your credit score.

Yes, it may be possible that you will qualify for a new loan if you settle a loan, but it may be more difficult to obtain approval for a new loan initially. You may need to improve your credit score to show other lenders you are capable of repaying the money.

You may obtain your credit report from TransUnion CIBIL or an approved Credit Bureau in India to determine whether your account shows as terminated or settled. Your report will list all of your open and closed accounts, as well as your settled accounts.

Contact

care@zetapp.in

Social

Build and Maintain a 750+ Credit Score