December 11, 2025 · 9 mins read

Santosh Kumar

Credit cards have become a cornerstone of contemporary life, offering convenience, benefits, and on-the-spot purchasing capacity. But with all the bells and whistles Indian credit cards now come with, the option to convert purchases into EMIs is undoubtedly one of the most attractive. Just tap or swipe once and transform a big expense into bite-sized monthly instalments. It seems obvious, and in many ways, it is. But as with any financial instrument, a credit card EMI is valuable only when deployed judiciously, and dangerous when deployed recklessly.

If you’ve ever wondered how credit card EMI works, whether it is genuinely useful, or when it might be a mistake, this guide will walk you through everything you need to know. We will also explore how to use a credit card for EMI, the situations in which EMIs make sense, and the times when you’re better off avoiding them. The goal isn’t simply to demystify the mechanics, but to assist you in making a financially confident decision for each big buy.

Before deciding when to use or avoid an EMI facility, it’s essential to understand how credit card EMI works in the first place. When you opt for EMI on a credit card transaction, your bank permits you to repay that amount over a fixed term, typically three to twenty-four months, instead of the entire amount in the subsequent billing cycle.

Rather than pay off the balance in full straight away, your credit card breaks that purchase up into convenient monthly instalments. Each payment contains some principal (the purchase price) and interest. Though certain banks do provide partner retailer ‘No-Cost EMI’ options, the majority of EMIs are interest-bearing, and the rates differ by bank, card and purchase category.

Once the EMI is enabled, the bank debits the EMI amount on a monthly basis from your available credit limit. Fix rate, instalments. And over time, as you pay back those instalments, your credited balance refills. This is what sets credit card EMIs apart from personal loans or BNPL options, as the repayment cycle is tightly connected to the card's limit.

If you’re thinking about how to use an instant online credit card for EMI, the process is relatively simple today. You can redeem an eligible purchase via your banking app, Internet banking, customer care or even directly on the retailer’s payment page. A lot of big-ticket purchases like electronics, appliances, or airline tickets will automatically offer you an EMI choice at checkout.

The real question, though, is not how EMIs work, but whether they’re right for your wallet.

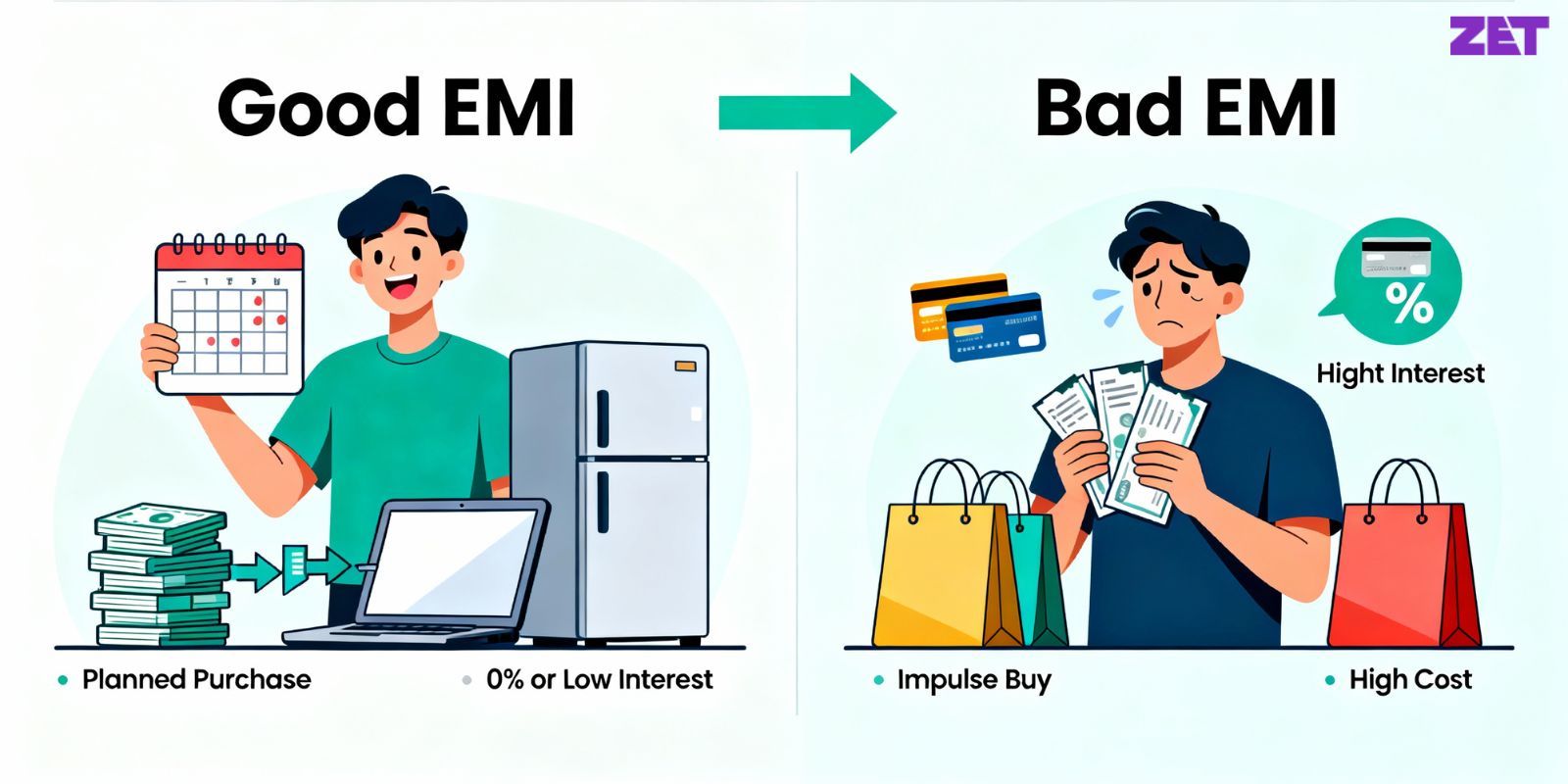

A credit card EMI is a fantastic tool to have in your arsenal. When you apply for credit card, choosing EMI isn’t just okay, it's usually smart money.

If you’re purchasing a high-ticket item, say, a television, laptop, sofa set or home appliance, and you're confident you can easily meet the instalments, an EMI simplifies your budgeting. Rather than shelling out a lot of money up front, you're amortising the cost with affordable monthly instalments.

This preserves your cash flow for critical monthly bills, emergency savings and investing — instead of boiling your bank account dry in a single blow. Amid all the hoopla about emotional spending, a lot of folks now opt for EMI deliberately as a budgetary device instead of borrowing under duress.

Sure, a 'No-Cost EMI' sounds good, but keep in mind that actual no-cost EMIs are provided only when the retailer or brand chooses to subsidise the interest amount. When the EMI is really zero-interest, and there are no sneaky fees, EMI is almost always a wise choice.

For instance, several smartphone brands, electronics stores and online marketplaces provide authentic no-cost EMI offers during festivals. And when it does, a spread payment over three or six months is usually more convenient than an upfront payment.

Even if you have the money to pay, an EMI can help you keep your savings intact, particularly if you’re striving towards a financial goal like an emergency fund, SIP or travel. Let’s say you’re paying ₹30,000 upfront for a laptop, you could opt for a 6-month EMI and invest the difference at your own rate.

Of course, this only works if the EMI is cheap and doesn’t have a high interest rate.

Credit card EMIs are typically lower than revolving credit (i.e., balance carry forward) or cash advances from credit cards. They can also occasionally even be less expensive than personal loans. If the buy is unavoidable and you don’t have enough cash on hand today, an EMI may be a more disciplined repayment path than other high-interest debt options.

EMIs sound innocent enough, but sometimes they silently conjure up long-term debt traps. These are the times you really need to reconsider turning every buy into EMI.

This is maybe the greatest risk of EMIs. Because they make costly products appear cheap in monthly payments, they frequently cause people to purchase stuff they neither need nor can afford. A ₹60,000 phone seems less scary when it’s spread out over twelve ₹5,000 instalments, even if it ends up costing more because of the interest.

Once EMI is an excuse for compulsive shopping, it can rapidly throw your financial life off track.

At least some EMI conversions have interest rates of 14% to 24% per annum. In these cases, the total amount paid over the tenure could be significantly more than the sticker price. If the purchase is not vital or immediate, it is better to save and buy later rather than tie yourself down to a high-interest EMI.

Banks can tack on processing fees, conversion charges, or GST, taking it a step further. Just always compute the repayment amount before deciding.

And if your current EMIs already devour a good chunk of your monthly income, adding one more just hypes up this pressure. Over-committing can cause you to miss payments, incur late fees, or hurt your credit score. The financial turmoil over the next decade could exceed the ease of having it now.

If you're between jobs, anticipating a career shift, or dealing with sporadic income, an EMI might not be such a great idea. Even a relatively minor monthly obligation is onerous in these fiscally murky waters. Better to stick with your plan to wait until your income stabilises before you add a new obligation.

EMIs block your credit limit temporarily. For instance, if you purchase a ₹50,000 product on EMI, your credit drops by ₹50,000 and gradually unblocks as you pay instalments. This limits your use of the card for emergencies or everyday purchases. If you’re living on your card for day-to-day expenses, a long-term EMI could throw off your monthly budgeting.

Understanding how to use a credit card for EMI is not just about the process but about making the right financial choice. Things to check before choosing EMI.

1. Check the interest rate and total repayment amount.

2. Explore no-cost EMI offers.

3. Choose shorter tenures to reduce interest.

4. Make sure your monthly budget can accommodate the instalments!

5. Steer clear of EMI for aspirational or impulse buys.

6. Monitor several EMIs to steer clear of debt.

When used cautiously, credit card EMIs can help you keep your finances in check. When used carelessly, they can drag you into long-term debt.

Credit card EMIs are a potent financial instrument, not inherently good or bad. They can provide flexibility, convenience and breathing room in large purchases. But they can also tempt you to overspend, generate wasteful debt, and stress your budget each month if wielded indiscriminately.

Understanding how credit card EMI works and recognising your own spending patterns is the key to making the right decision. Employ EMIs wisely, shun them when frivolous, and eternally make sure they nestle snugly with your fiscal aims.

1. Is no-cost EMI really free?

That is, only if the retailer and bank eat the interest completely. Just READ the terms – you don’t want them sneaking in a daily surcharge or jacking up your product prices!

2. Will converting to EMI impact my credit limit?

Yes. The amount you buy decreases your limit and refreshes over time as you pay back the instalments.

3. What if I default on an EMI?

If you default on an EMI, you’ll also be hit with late fees, interest, and possible credit damage.

4. Can I foreclose/cancel an EMI?

Most banks permit foreclosure, but a few may levy a nominal fee. The balance will be charged to your next statement.

5. What is Credit card EMI vs a personal loan?

Based on interest rates, tenure and urgency of purchase. Credit card EMIs are convenient for smaller buys, while personal loans tend to be cheaper for bigger loans.

Contact

care@zetapp.in

Social

Build and Maintain a 750+ Credit Score