March 15, 2025 · 19 mins read

Santosh Kumar

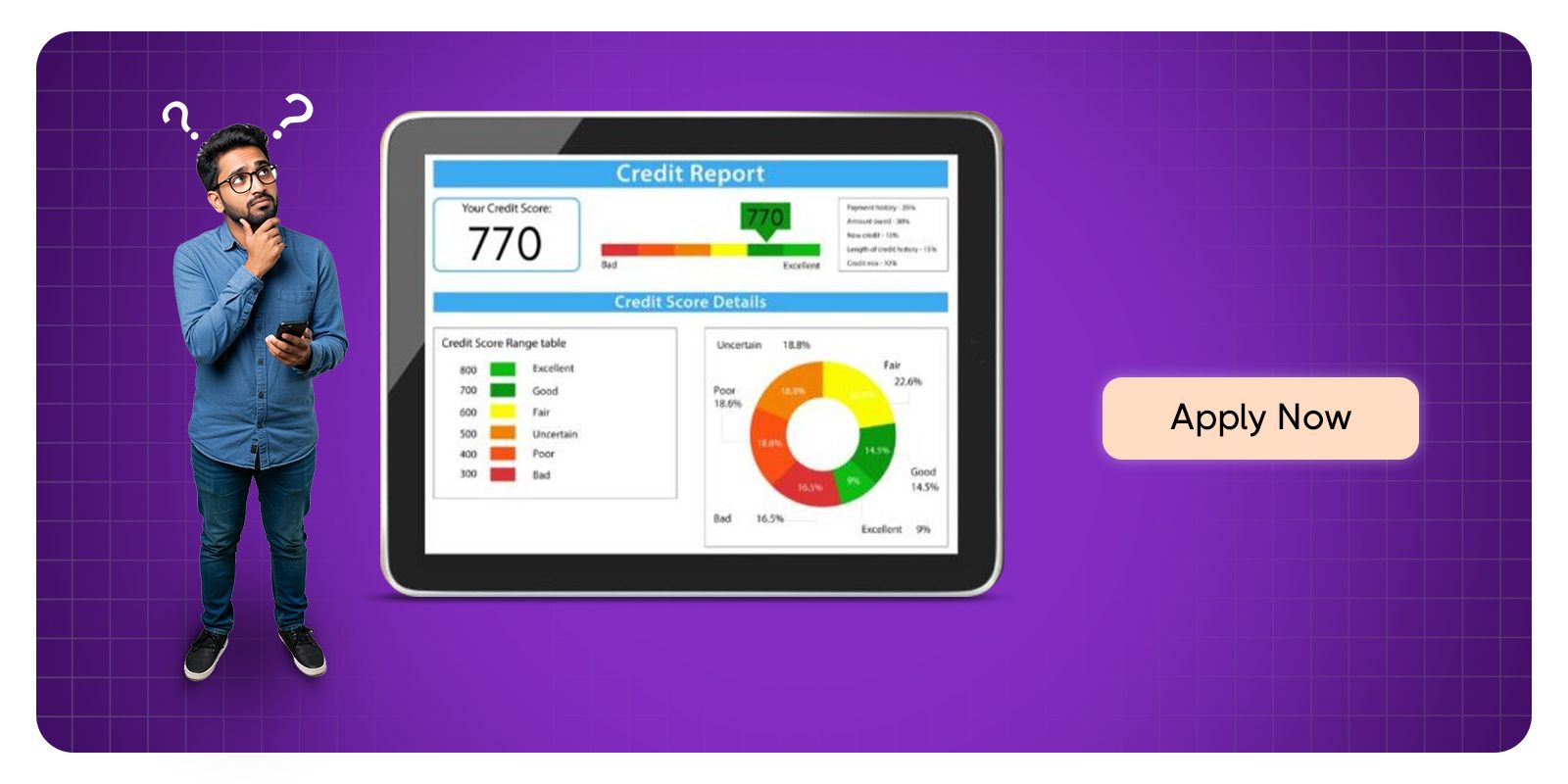

Your score falls within the range of scores from 740 to 799, which is considered Very Good. A 770 FICO® Score is above the average credit score. Consumers in this range may qualify for better interest rates from lenders. Approximately 1% of consumers with Very Good FICO® Scores are likely to become seriously delinquent in the future.

The highest score possible is 850 while the lowest is 300. In reality, achieving a credit score of 850, which is "exceptional" is fairly rare. It would take a perfect combination of many factors to get there.

The ideal credit score to get you the best interest rates, payment terms, and perks that come from being rated among the best of the best is above 760. Credit scores of between 740 and 799 are considered "very good."

For many people, achieving a "very good" score will take concerted financial steps and patience. Even if you don’t have a credit score of 760 or above, you can still have financing options available to you with a "good" credit score, including some with competitive rates.

As you can see, a 770-credit score is considered good by VantageScore standards and very good by FICO standards.

Falling in these ranges usually indicates responsible credit management and a higher likelihood of obtaining credit at more favourable terms. A 770 credit score can demonstrate creditworthiness to lenders, and you are likely to qualify for competitive interest rates and terms. You may even be able to have opportunities to take out credit cards with more premium perks. Bear in mind, however, that credit scores are not the only factor that is evaluated for these financial opportunities. Let's explore this in more detail below.

Read More:: MDR Charges on Rupay Credit Card

Credit scores can be thought of as a secret language of your financial life-an invisible number that could mean a ticket to your dream home, car, or easier loan approval. Yet, given they hold such importance, many are silenced with myths, misconceptions, and half-truths that embroil people into confusion, worry, or really worst, concrete ill financial decisions. From perpetrators of the myth stating one checking his own credit score would lower it to thinking that carrying a small balance is better than paying it off, many of these myths go unnoticed yet have the capacity to undermine one's financial well-being.

The credit score function is one not commonly understood. It is all about what the scores meant differently based on their numeric thresholds and how those numbers are interpreted by lenders; thus it is always advisable to become an informed consumer. Knowledge is power: with credit scores, however, it can also help avoid costly mistakes.

The myths must be dispelled and the realities behind credit score ranges exposed if there is any hope of transcending fear and uncertainty into clarity and confidence. Knowing what the numbers mean is the first step to financial freedom in building credit for the first time, repairing poor scores, or fine-tuning the present financial condition.

With a good/very good credit score, you may qualify for competitive interest rates on loans and credit cards than individuals with lower credit scores. For example, you may be able to take out more premium credit cards than someone with a lower score. These cards may even come with lower annual percentage rates (APRs). Note, however, that many premium cards come with higher annual fees, so it’s important to check this as you take out new credit cards.

Additionally, your chances of qualifying for auto loans and mortgages are better than someone with a lower credit score. Let’s discuss this further below.

Purchasing a car may be possible with a 770-credit score, but it’s important to note that different dealerships and lenders may use different credit scoring models and different scales to make their own loan decisions, which could impact your loan terms and approval odds.

Even with a “good” credit score, you may be declined, subject to higher interest rates or need to provide a larger down payment than if you had a higher credit score.

To help improve your chances for approval, it is generally beneficial to add a co-signer to the loan-if the lender allows—to share financial responsibility. Take note that while important, your credit score is just one of several factors lenders take into account when approving a loan.

Read More:: Rupay Credit Card UPI Charges

Buying a home with a 770 credit score may be possible, but it may be more challenging than if you had an excellent credit score. Some lenders may require a larger down payment, charge higher interest rates or have stricter loan terms.

Whatever you decide, carefully review and compare different lenders and loan options to find the best fit for your specific circumstances. Remember, credit scores are just one of several factors lenders use when approving home loans.

1: Even though a 770 credit score may grant you access to credit opportunities, you might feel motivated to take things to the next level. You may want to be extra diligent to boost your score from 770 to 800 and beyond.

2: First, remain proactive. That means keep doing what you’ve likely already been doing to obtain your current score. This includes paying bills on time and keeping your credit utilization ratio low.

3: Next, consider the following tips to help improve your score:

4: Monitoring your credit report for any signs of suspicious financial activity and taking action if you find inaccuracies by reporting them to the credit bureau(s).

5: Protecting your information, such as your Social Security number (SSN), from potential identity theft.

6: Diversify your credit mix by taking out a different type of credit (for example, a personal loan instead of another credit card) to showcase your ability to manage multiple types of accounts. Note that your score may dip temporarily due to lenders having to run a hard inquiry.

7: Consider enrolling in Chase Credit Journey®, a free online tool anyone can use to check their credit score without impacting it. You may also use the credit score improvement feature. With this feature, you can receive a personalized action plan, provided by Experian™, based on your credit behaviours and credit score goal to help improve your credit score over time.

8: Managing your debt-to-income ratio. This means that even if you get a salary increase or take on an extra source of income, try to keep your spending low.

Read More:: How does UPI Mandate Work

There are many different credit scores because credit scoring companies continually update and sell their scores to lenders.

Lenders use credit scores to make lending and account management decisions, such as who to approve and whether to change your credit limit. For the most part, lenders can choose which model they want to use.

FICO and VantageScore create and sell different credit scoring models, and both companies periodically release new versions of their credit scores-similar to how a software company might offer a new operating system.

The latest scoring models might incorporate technological advances or changes in consumer behaviour. Lenders can then decide to upgrade to a newer model or to stick with the older version that's already integrated into their systems and processes.

Read More:: How to Check CIBIL Score on Phone Pe

On revolving credit, Utilization, or usage rate, is a measure of how close you are to "maxing out" credit card accounts. You can calculate it for each of your credit card accounts by dividing the outstanding balance by the card's borrowing limit and then multiplying by 100 to get a percentage. You can also figure out your total utilization rate by dividing the sum of all your card balances by the sum of all their spending limits (including the limits on cards with no outstanding balances).

Most experts recommend keeping your utilization rates at or below 30%-on individual accounts and all accounts in total-to avoid lowering your credit scores. The closer any of these rates get to 100%, the more it hurts your credit score. Utilization rate is responsible for nearly one-third (30%) of your credit score.

More than one-third of your score (35%) is influenced by the presence (or absence) of late or missed payments. If late or missed payments are part of your credit history, you'll help your credit score significantly if you get into the routine of paying your bills promptly.

If you manage your credit carefully and stay timely with your payments, however, your credit score will tend to increase with time. In fact, if all other score influences are the same, a longer credit history will yield a higher credit score than a shorter one. There's not much you can do to change this if you're a new borrower other than be patient and keep up with your bills. Length of credit history is responsible for as much as 15% of your credit score.

Read More:: What is YBL in UPI?

The FICO® credit scoring system tends to favour multiple credit accounts, with a mix of revolving credit (accounts such as credit cards that enable you to borrow against a spending limit and make monthly payments of varying amounts) and instalment loans (e.g., car loans, mortgages and student loans, with set monthly payments and fixed payback periods). Credit mix is responsible for about 10% of your credit score.

People with Very Good credit scores can be attractive targets for identity thieves, eager to hijack your hard-won credit history. To guard against this possibility, consider using credit monitoring and identity theft protection services that can detect unauthorized credit activity. Credit monitoring and identity theft protection services with credit lock features can alert you before criminals can take out bogus loans in your name.

Credit monitoring is also useful for tracking changes in your credit scores. It can spur you to take action if your score starts to slip downward and help you measure improvement as you work toward a FICO® Score in the Exceptional range (800-850).

Read More:: How to add money in Phone Pe wallet?

There’s no one path you can follow to get an excellent credit score, but there are some key factors to be aware of while you continue to build and maintain it.

Even if you’re holding steady with excellent credit, it’s still a good idea to understand these credit factors - especially if you’re in the market for a new loan or you’re aiming for the highest score.

Your credit utilization rate is calculated by dividing the amount of credit you’re using by the amount of credit available to you. You should try to keep this under 30%, but usually, the lower your utilization rate, the better.

Having high credit limits and keeping your credit card balances low are two ways to help your credit utilization. If you need to lower your credit utilization quickly, you can ask your credit card issuer to raise your credit limit but know that it might result in a hard inquiry.

If you’re planning to apply for a new card in the near future and you’ve got a high credit utilization rate, consider making some early payments on your existing card balances first. If you pay down your balances before they’re reported to the credit bureaus, it could help you get your credit utilization rate as low as you can and potentially boost your scores before you send in that new application.

Read More:: How Much Money Can We Transfer Through PhonePe?

Your payment history is an important factor in your credit health. A single late payment can potentially have a big impact on your scores.

If you’ve missed a due date, it could be worth giving your credit card issuer a call to ask if it will remove the late payment, especially if that’s never happened before.

Another way to demonstrate your experience using credit is by showing lenders that you can juggle different types of credit. This could include credit cards, which are a type of revolving credit, as well as loans like mortgages that you pay in instalments.

We generally don't recommend applying for a loan just to build your scores, though, especially if it's going to cost you money. Also, applying for a new loan can mean a hard inquiry is logged on your credit reports, which can affect your credit.

Another factor weighed in your credit scores is the age of your credit history or how long your active accounts have been open.

Cancelling a credit card can affect the age of your credit history, especially if it’s a card you’ve had for a while, so weigh that potential impact when you’re deciding whether to close a card. Only time can offset the impact of closing an older account, but you’ll also lose the credit limit amount on a closed card, which can negatively affect your credit utilization rate.

Heads up that card issuers may decide to close your accounts if you’re not actively using them, so make sure you keep any accounts you don’t want closed active with at least an occasional minimal purchase.

Read More:: Difference Between RuPay Credit Card and Visa Credit Card

Even though credit scores may appear to be nothing more than numbers, they can truly impact your financial opportunities and possibilities. Credit scores range from 300 to 850 and can be categorize which allows lenders to assess whether they can lend money to you. Credit scores between 300 and 579 are considered poor and lenders usually deny people in this range loans or credit cards or charge them extremely high interest rates. If you can achieve at least a credit score of 580 and below 669 you are in the fair category. In the fair category people should still be able to get credit, but possibly with stricter terms.

The range of 670-739 is considered good. Borrowers in this good category are generally approved for loans and often, receive competitive interest rates. The range of 740-799 is very good. In this range, lenders consider you a low risk and will provide you with more favorable offers and premium options with credit products. The range of 800 and up is excellent. In this excellent range, you'll have access to the best financial products, as well as premium credit cards and the most favorable interest rates.

These ranges are important because they affect nearly every financial decision you have to make, from buying cars or houses to applying for personal loans. And knowing where you stand allows you to have meaningful goals and puts you in a position to take targeted steps to improve your financial profile, leveraging your score as a successful tool.

Here are some tried and true behaviours to keep top of mind as you begin to establish—or maintain—responsible credit behaviours:

1: Pay your bills on time, every time. This doesn't just include credit cards—late or missed payments on other accounts, such as cell phones, may be reported to the credit bureaus, which may impact your credit scores. If you're having trouble paying a bill, contact the lender immediately. Don't skip payments, even if you're disputing a bill.

2: Pay off your debts as quickly as you can.

3: Keep your credit card balance well below the limit. A higher balance compared to your credit limit may impact your credit score.

4: Apply for credit sparingly. Applying for multiple credit accounts within a short time period may impact your credit score.

5: Check your credit reports regularly. Request a free copy of your credit reports and check them to make sure your personal information is correct and there is no inaccurate or incomplete account information. Free online weekly credit reports are available at www.annualcreditreport.com. Remember: checking your credit reports or credit scores won't affect your credit scores.

Checking your credit score right before you apply for a new loan or credit card can help you understand your chances of getting approved and qualifying for favourable terms. But regularly checking it further ahead of time gives you the chance to improve your scores and possibly save hundreds or thousands of dollars in interest.

You can check and monitor your FICO® Score and credit report for free from Experian with daily updates and real-time alerts for suspicious changes in your report. A free account also offers free credit-building features, like Experian Boost, and insights into your credit history and score.

A 770 credit score is Very Good, but it can be even better. Boosting your score into the Exceptional range could let you qualify for the very best interest rates and terms. A great starting point is to get your check your credit score to find out the specific factors that impact your score the most. A strong credit score can open doors to better financial opportunities. So, it’s very important to keep track of your credit health. You are likely already well on your way to solidifying a positive financial foundation for yourself. You've probably developed healthy habits and consistency. Now, you have to protect it, meaning you must remain proactive when it comes to monitoring your credit. It could take some time to improve your score further.

A CIBIL score of 730 is considered good.

Yes, a 770 credit score qualifies you for credit cards.

A 770 credit score can help you secure loans with favourable terms.

Continue practising good credit habits to maintain or improve your score.

It’s advisable to look at your credit score every three months. This way you can correct any errors, spot any potential identity fraud or theft of your credit information, and track how much you have improved since your last review. Don't worry, when you check your credit score, it is a "soft inquiry" and does not impact your credit.

Credit utilization means how much credit you have used is a percentage of your total credit. Most experts believe a credit utilization ratio is best to stay less than 30%. For instance, If your total limits is ₹1,00,000 you want to try to keep it below ₹30,000. A lower utilization ratio will help reassure banks and lenders you can manage your credit.

Improving your credit score takes time and patience. Making timely payments, reducing debt, and keeping utilization down will take some effect in a few months. Just remember to allow up to 6-12 months before significant improvement is likely depending on the score and habitual behavior observable to lenders. Popular saying is "it can take time" to show any consistency in improving your credit score.

Absolutely. Hard inquiries occur when lenders conduct a credit check, either for a loan or a credit card. While just a few hard inquiries will have only a modest, and temporary, effect on your credit score numerous inquiries in a short time period could indicate a higher risk of default and slightly affect your score.

Falling behind on a loan payment, failing to pay on time, closing an old account, using all of the available credit on a card, or missing a payment can negatively affect your credit profile. If you focus on avoiding these behaviors, you will significantly improve your credit profile.

Paying off debts will have a positive impact on your score. When a consumer pays off debts they are usually increasing their payment history, lowering credit utilization and indicating risk characteristics associated with consumers who resolve debts. Managing debts in a responsible way is one of the quickest and most effective ways to build a solid credit profile in India.

Yes. FICO, Vantage Score, and CIBIL scores may balance different factors, such as payment history, length of credit and utilization differently. The numbers might differ a little bit, but good credit behavior is effective across all scoring models.

Contact

care@zetapp.in

Social

Build and Maintain a 750+ Credit Score